$ABA: The "Batangas Bargain"

$ABA: The "Batangas Bargain"

10% dividend yield, 40% discount to book value, and unlikely growth potential.

Before we get started, please consider subscribing to the newsletter. That way, you will receive the newsletter straight to your email inbox and you will not need to scroll through the entire internet just to see or find my most recent posts.

You can type your email in the text box and hit “Subscribe.” Thanks! Now, onto our analysis of $ABA…

With a 10% dividend yield, the stock selling at a 40% discount to book value per share, and management allocating capital to revenue-generating projects, $ABA looks undervalued.

Whenever I’m investing, I always try to look at the downside. AbaCore Capital Holdings, Inc. is selling at a price level which I think offers investors sufficient protection from possible loss and underperformance.

To be honest, I don’t think $ABA will win any “highest quality stock in the PSE” polls. But in the same way a great business can be a bad investment if you overpay, a mediocre company can have adequate upside if you pay a bargain price for it.

I believe $ABA’s stock, at its current price of Php 2.16 per share (Php 9.1B market cap), is one such compelling investment opportunity.

I have to tell you though that this is not a write-up or a report. This is just a collection and aggregation of my notes and thoughts on the company. I’m not looking to give you any advice. I am not your financial or investment advisor. I’m only telling you what I think thus far and my opinions can change when presented with compelling new information. Not to mention that I could have missed a lot of important facts about the company. So, be careful and don’t invest solely based on this post. Do your homework.

On that note, let’s dive in…

Business Overview

AbaCore Capital Holdings, Inc. (ACHI) is a holding company with interests in “financial services,” real estate, gold and coal mining, and leasing of gaming equipment.

As of September 2022, below are the company’s following subsidiaries:

“Financial services”: Wholly-owned Philippine Regional Investment Development Corporation or “PRIDE.”

Real estate: Omnicor Industrial Estate and Realty Center, Inc. (100% subsidiary of PRIDE); Kapuluan Properties, Inc. (100%-owned); Vantage Realty Corporation (100%-owned).

Gold mining: Abacus Goldmines Exploration and Development Corporation or “AbaGold” (99.70%-owned).

Coal mining: Abacus Coal Exploration and Development Corporation or “AbaCoal” (100%-owned).

Leasing of gaming equipment: Pacific Online Systems Corp. (4.89%-owned).

Developing a deep understanding of the economics of the company’s business lines and respective subsidiaries may not all be that useful and may even be irrelevant given that most of the subsidiaries’ revenues come from selling land parcels and gains on fair value adjustments on land assets & mining rights. Its coal and gold mining businesses are even in the “pre-operation” stage. See each segment’s business results below:

“Financial Services”

Its “financial services” segment is represented by its 100% ownership in Philippine Regional Investment Development Corporation or “PRIDE.” I put the quotation marks for a reason. It is because PRIDE doesn’t really provide any financial services to anyone. It mostly provides its “services” to ABA-affiliated companies. Its primary line of operations is providing “project financing” for a variety of real estate, logistics, and infrastructure projects (mostly projects by subsidiaries and affiliates of ABA).

An important fact to note about PRIDE is that ABA is looking to list PRIDE in the PSE “by way of introduction.” From PinoyMoneyTalk: “In Listing by Way of Introduction (LBI), the company listing shares does not anymore have to undergo the lengthy book building, underwriting, and public offer process [that IPOs have to go through]. Instead, upon PSE approval of its LBI listing application, the company’s stocks are automatically listed on the exchange and immediately [start] trading.”

Last June 2022, shares of PRIDE have also been declared to be distributed as stock dividends to ABA shareholders to make the listing possible.

Real Estate

Though it is under PRIDE, Omnicor Industrial Estate and Realty Center, Inc. houses most of ABA’s real estate activities.

It owns a 52% stake in Montemaria Asia Pilgrims, Inc. (MAPI). A non-profit pilgrimage site and membership club that issues proprietary and associate shares which intends to go fully operational once quarantine restrictions are lifted. Montemaria includes a giant statue of the Blessed Virgin Mary, chapels, auditoriums, retreat houses, meditation gardens, condotels, and other facilities.

According to the company, through their subsidiaries, they hold substantial land assets around the Montemaria project which they can of course either sell or develop projects on.

Omnicor may house most of ABA’s real estate activities, but it does not house, to the best of my knowledge, ABA’s land parcels that the company generates most of its current “income” from.

Those land assets might be held by its other real estate subsidiaries Kapuluan Properties, Inc. and/or Vantage Realty Corporation.

Gold & Coal Mining

Both AbaGold and AbaCoal are still companies with no business operations.

The one thing AbaGold currently has going for itself is the fact that it owns 102 gold mining claims in San Franciso and Rosario, Agusan del Sur, and Barobo, Surigao del Sur. Based on the appraisal report of an independent appraiser in 2011, the estimated fair value of its gold mining rights is around ~P2.6B. Of course, fair value estimates are not that reliable and you should be careful when making it a big factor in your investment decisions.

Meanwhile, AbaCoal is currently looking to monetize its coal deposits via a joint venture with Oriental Vision Mining Philippines (ORVI): (emphasis mine)

“So far, in 2022, ABA is pursuing ventures with various business partners across a range of sectors. In mining, the company signed a coal exploration agreement with Oriental Vision Mining Philippines Inc. (“ORVI”). Under this agreement, ORVI will conduct exploration work on three coal blocks ABA owns in the province of Surigao del Sur. ABA will earn royalty fees should ORVI find coal and other minerals in the course of its exploration work. Overall, ABA has a coal concession worth 7,000 hectares.” (Manila Bulletin)

“In July, Abacoal sealed a deal with Oriental Vision Mining Philippines Corp. (ORVI) to start developing coal mines in the province (Surigao Del Sur) covering 3,000 hectares. ORVI had committed to developing these blocks within six to 12 months.” (Inquirer)

Essentially, ORVI will do the heavy lifting while AbaCoal just has to sit pretty earning royalties.

Leasing of Gaming Equipment

AbaCore owns a 4.89% stake in the publicly listed lessor of online betting equipment to PCSO’s Visayas and Mindanao operations: Pacific Online Systems Corporation (POSC). PCSO is the official government entity that facilitates the lottery in the Philippines.

POSC currently leases to PCSO an online network of approximately 4,500 betting terminals selling various lottery games operated by PCSO. Total Gaming Technologies Inc, POSC’s 99-percent owned subsidiary, leases to PCSO an online network of approximately 1,500 betting terminals which the latter uses for its Keno games. POSC has been a systems provider for the PCSO since 1996.

Since POSC enjoys an exclusive right to lease betting equipment to PCSO in Visayas and Mindanao, it faces minimal competition. Last December 1, 2021, POSC and its venture partners signed a Memorandum of Agreement with PCSO for a five-year lease agreement for the Customized PCSO Lottery System that PCSO will need for its PCSO Lottery System (PLS) — PCSO’s proposed nationwide online lottery service.

Regarding its traditional betting terminals though, recent company press releases only point to equipment lease agreements being extended until April to July 2022. I still haven’t found any documents, news reports, or company press releases regarding any equipment lease agreements being extended.

Current Business Model

To make it short, ABA’s current business model is selling its land assets and using the proceeds to pay a 10% dividend yield and investing in projects that can generate recurring revenues for the company.

The company has no income coming from direct business operations. Almost all of the accounting earnings it reports are from gains on selling its parcels of land and increases in the fair value estimates of the other land assets they own and the mining rights its gold and coal mining subsidiaries have. It is generating negative operating cash flows with “Gain on fair value adjustments” being worth almost ~98% of its net income in 2021.

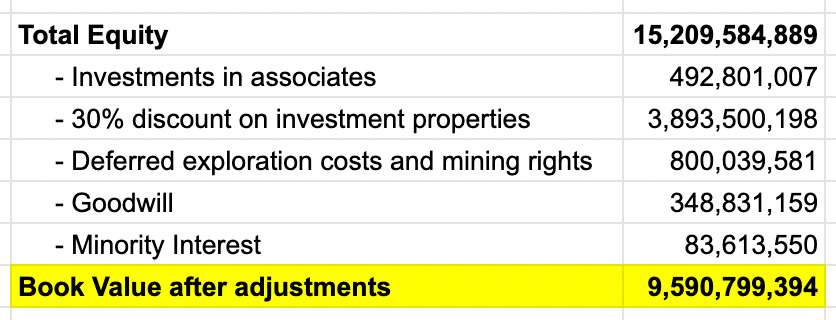

Since its earnings quality sucks, we’ll be valuing the company based on its assets. We can invest in the company with the net assets in mind rather than its future earnings or cash flows because management has been unlocking the value of its assets.

Our hope is that, with ABA’s management converting the holding company’s assets into cash and paying the proceeds to shareholders or investing it in projects that can generate recurring revenues, we can have confidence that we’re not buying into a value trap.

Batangas’ Growth

Most of ABA’s land assets are located in Batangas. CALABARZON (Cavite, Laguna, Batangas, Romblon, Quezon) or Region IVA is one of the most rapidly-growing regions in the Philippines, second only to the National Capital Region (NCR) in terms of Gross Regional Domestic Product (GRDP) in 2018.

In 2021, CALABARZON had the highest share of industrial output (at 25.1%) in the country. In the region, Batangas is the third largest behind Laguna at first and Cavite in second.

Batangas City is also home to the country’s third-largest port, the Batangas International Port, and is also a beneficiary of government tax incentives that aim to lure businesses out of the heavily congested Metro Manila.

In addition, CALABARZON’s tourism sector has been growing as well with Batangas being the third-most visited province in the country last 2018. Its proximity to Metro Manila makes it an attractive place for both tourists and locals looking to have a vacation.

All in all, Batangas’ robust industrial and manufacturing growth, growing tourism market, and improving economic connectivity due to the Philippines’ infrastructure build-out under the previous administration’s Build-Build-Build (BBB) program are all helping grow the value of land in the area.

The Balance Sheet

An investment thesis in $ABA will rely heavily on the strength and characteristics of ABA’s balance sheet. You have no consistent earnings from operations nor any cash flows to rely on, all you have going for you will be the company’s assets:

Investment properties make up almost ~74% of the company’s total assets with property and equipment coming in second at only ~10%. Almost all of its Php 12.9B in investment properties are land parcels it owns in Batangas.

We can thank the growing economy of Batangas and the CALABARZON region for the growth in fair value. Management has also noted that its “fair value adjustments” only partially reflect the company’s growing property values and expanding property base. This is because, under the accounting standards of the Philippines on Holding Companies, fair value adjustments are done only on a portion over the entire property portfolio of the company. So, ABA’s real book value might actually be higher than what is being presented in its financial statements, and investors, at current prices, could be buying with a supposedly wider margin of safety than they might think.

Based on ABA’s estimates last April 2020, the market value for its investment properties is around Php 4.77 per share. As of Feb. 2023, $ABA shares are only trading at around Php ~2.30 per share. Assuming management’s estimates are correct, this presents a large margin of safety. With the land appraisals being “conservative” and “outdated,” the lands’ true economic value may differ from what is being presented in the financial statements.

I try to have the belief that fair value adjustments should be held as illusionary until proven otherwise. Even if ABA has sold some of its land parcels at higher prices than was recorded on its balance sheet and management has provided proper reasoning for why its investment properties should be valued higher (imperfect accounting standards & Batangas’ growth), we would be served well by putting a discount on its supposedly valuable assets. We don’t know if the figures are inflated and how inflated they could be. It’s better to be pessimistic than sorry.

Currently, ABA’s market cap is Php 9.1B. If you buy now, you’ll be buying at a price below what the book value of the company would be if its stakes in POSC, AbaGT, and PSDBI were worthless, its mining rights producing poor returns, and if its land assets were worth 30% less. The company has little to no debt as well.

All that while ABA’s management is selling the land parcels and investing the proceeds in projects that can generate recurring revenues.

Prospects

The good thing about ABA is that its management acknowledges the reality that the holding company is in (that it has no operating income and only has land assets going for itself) and doing reasonable things to unlock value for shareholders.

Through PRIDE, ABA entered into a joint venture with Highsource Prime Building, Inc. (Highsource) to develop a four-star hotel, a land and water amusement park with supporting facilities, 3D Glass Paradise, a residential community and commercial establishments to be located at the Montemaria Project in Pagkilatan, Batangas tourism site:

“Highsource will invest up to 400 million US dollars in the development. The project with Highsource will have 2 phases. In the first phase, PRIDE will contribute to the joint venture the mountain top land of its subsidiaries overlooking Batangas bay and the verde island passage located at Pagkilatan, Batangas City with a total area of 17 hectares at 9,000 pesos per square meter for a total value of 1.6 billion pesos for at least 40% share in the joint venture. On the other hand, Highsource will invest up to 2.6 billion pesos in cash and development for the first phase – with increasing share in the joint venture as it reaches certain milestones.

The second phase will have PRIDE contribute another 20 hectares of mountain top land of its subsidiaries at the reappraised value at the time of commencement of phase 2 for a minimum of another 40% while Highsource will contribute the proportionate amount in cash or development.

Considering the quick appreciation of property values in Batangas, especially for tourism-oriented land near the beach front or along the shore, both parties have agreed that any delay in development will allow PRIDE to have its land reappraised to updated market values and adjust higher the actual value of its land contribution to the joint venture which could increase its share in the joint venture.” Source: PSE EDGE

As mentioned earlier, ABA also has its AbaCoal-Oriental Vision Mining Philippines (ORVI) coal exploration joint venture where ABA, through AbaCoal, can unlock the value of its coal assets in Surigao Del Sur through the royalty fees ORVI will be paying out over the course of its exploration work.

ABA will be building an “Energy Hub” in Batangas too, called “Aba Energy Hub” located in Simlong Batangas City. Through Simlong Energy Development Corp. (SEDCO), which ABA is set to acquire a 90% stake in, ABA is looking to lead the development of the hub. The energy hub will be an industrial location for energy-related projects like power plants and liquid natural gasification projects.

PRIDE also has a partnership with SquidPay Technologies. The partnership aims to convert PRIDE’s subsidiary, PhilStar Development Bank, into a Digital Bank based in the province of Batangas. In their June 22, 2021 press release, ABA announced that PRIDE is expecting to book a profit from the Philstar-Squidpay digital bank partnership.

Though these projects might look good on paper and ABA might still have other joint ventures in its pipeline, I don’t think you should expect too much from them. Not because they might not work out (although they really might not), but because a lot of unexpected things can happen. ABA has had other joint ventures before that did not bear any fruit and were ultimately terminated.

Lower your expectations. It is people that do business. People will be people.

Management

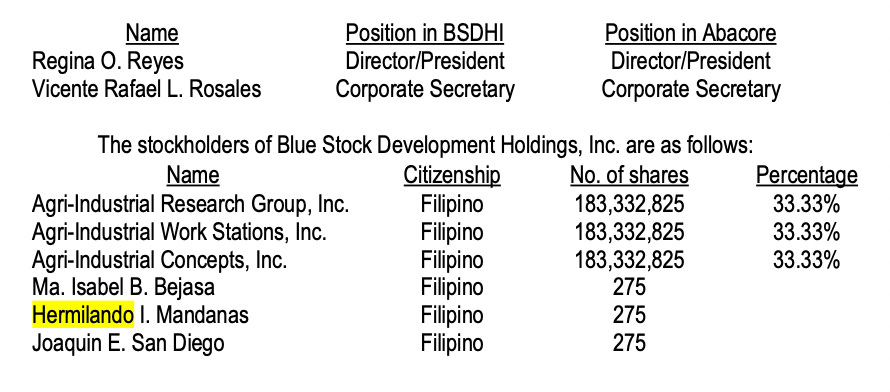

Regina O. Reyes used to be ABA’s President and CEO. She was instrumental in leading the company as she was voting for the shares owned by Blue Stock Development Holdings, Inc. (BSDHI) and Hedge Integrated Management Group, Inc. (HIMGI), that have ownership in ABA of 20.68% and 31.95%, respectively. Ms. Reyes had significant skin in the game; she was chairman of both BSDHI and HIMGI (HIMGI is a wholly-owned subsidiary of BSDHI).

Unfortunately, however, Ms. Regina O. Reyes passed away on the 5th of May, 2022. Under her tenure, ABA was able to win the Simlong Energy Industrial Park project in Batangas (or “ABA Energy Hub”).

Before we get into the new Chairman and CEO of ABA, it must also be noted that the founder of ABA and husband of Ms. Reyes, Mr. Hermilando I. Mandanas, is the current governor of Batangas since 2016 and is a shareholder of BSDHI—though it is stated that he only owns 275 shares. He most likely remains to be an important asset for ABA.

Given Ms. Reyes’ unexpected demise, ABA’s board of directors unanimously voted to appoint Mr. Raul B. De Mesa, ABA’s chairman, as the company’s new President and CEO. He will also be serving in the company’s Risk Management and Compensation and Remuneration Committees.

Mr. De Mesa has been sitting on the board since 2014 and has been Chairman since 2017 when Mr. Hermilando I. Mandanas had to step down as he was appointed governor of Batangas. Mr. De Mesa, according to filings, only owns 13 shares of ABA. He’s a banker, having served as Bank of Commerce’s President and CEO and later Chairman. Overall, he is said to have 37 years of experience in the financial sector.

Mr. De Mesa looks like a promising fellow, but I would be lying if I said I know what his appointment will mean for ABA shareholders. One of his first moves though has been the distribution of PRIDE shares as share dividends to ABA shareholders to make PRIDE’s listing on the PSE “by way of introduction” possible. Regarding his alignment with common stockholders, all public filings and information I have come across so far only point to him owning 12 to 13 shares of ABA.

Dividend History

When you look at ABA’s dividend history, it only really started picking up the pace again in 2019 when it paid a 20% cash dividend worth Php 637M in total.

It had paid dividends before 2019, but the most recent was six years prior (2013).

The dividends it declared in 2020 were supposed to be a 10% cash dividend, but the Board amended it to a 10% share dividend instead citing pandemic reasons. Once regulatory approval from the SEC is secured, only then will the 10% share dividends be paid out. I don’t know why it has taken this long though.

Its 2022 PRIDE share dividends have still not been distributed for the same reasons:

"Both property dividends and cash dividends may only be paid after the SEC approves the Property dividends. To synchronize payments of both the Property and Cash Dividends, ABACORE shall apply with the SEC for a deferment of the regulatory payment date of dividends as provided under law."

ABA doesn’t have a long track record of consistently paying cash dividends. Though, in its board meeting last December 2022, the board has promised to maintain a dividend policy of not less than 10% every year (10% dividend yield). If $ABA declares a 10% dividend this 2023, it would most likely be a cash dividend rather than a share dividend or hybrid-type (share + cash) since management really was looking to pay 10% cash dividends prior to COVID but had to pivot to paying share dividends instead to make sure that it had enough buffer to meet the company’s capital requirements.

Hmmm… I like what I’ve been seeing from Mr. Raul B. De Mesa so far.

It’s too early though, I guess we’ll just have to wait and see how he manages ABA. Let’s hope they follow through on their commitments.

Liquidity Risk

ABA’s stock is very obscure and often trades at very low volumes. As of February 2023, the 30-day average volume of $ABA shares is only at ~12M shares or around Php 24M in value (~0.25% of market cap), so it might take a while before the stock gets revalued to what could be its fair value.

Foreign investors have been taking note of ABA though. On September 19, 2022, Auerbach Grayson & Company, a New York-based global brokerage and investment bank, said that it had “successfully placed a block of stock” in ABA. They liked ABA management’s expansion plans and the stock’s discount to book value.

Another potential catalyst would be the 10% dividends that could be paid out this year 2023.

Having a catalyst is useful and reduces uncertainty, but given that ABA’s stock is selling at a bargain price relative to book value and its possible prospects, catalysts may just be a nice cherry on top rather than an essential.

The downside is well protected. Unless management messes up big time, the chances of a big decrease in ABA’s share price are close to zero. A stock already selling at a big discount to its assets that are said to be worth more than is currently being stated in the company’s accounting will most likely not go down any further. Although, of course, there may perhaps be a possibility. It is just very unlikely for $ABA to be going anywhere but up given enough time.

Conclusion

The common investor would avoid ABA given its convoluted story and corporate structure (not to mention its sketchy revenues and lack of cash flow). I am also wary of it as well, a lot about the company is very vague and abstract—I don’t like that.

But the investment thesis is simple: a holding company with supposedly valuable land has been liquidating it and using the proceeds to pay a 10% dividend yield and invest in projects that can generate recurring revenues down the line is selling for ~0.6x its net asset value.

There is a lot of uncertainty about the long-term upside and the future, but the margin of safety is wide given that its book value may be worth more than what is being currently reflected in the company’s balance sheet. A company with such characteristics, I think, should not be selling at such a discount to book value.

I would not bet the house on $ABA, but I don’t think it’s all too bad as well. It will take a patient and courageous investor to keep holding the stock. But what stock doesn’t?

Big thanks to Ots Bry and Ryle Mungcal for reading drafts of this post. I learned a lot from their feedback.

Lastly, please subscribe to the newsletter so you will get my posts straight into your email inbox. I’ll be posting a lot of “writeups” and commentary in the following weeks and months. It’s also free. Subscribe! :)